|

|

|

|

|

||

|

|

|

|

|

|

|

||

|

|

Second Cambodia

Development Cooperation Forum

The current financial crisis being witnessed in the United States and other developed countries is unprecedented since the 1930 Great Depression. Although it represents a major challenge for ASEAN and Asia as a whole, its impact on ASEAN economies is expected to be mitigated. Our region had gone through these painful experiences 10 years ago, when the Asian Financial Crisis swept through the region and left behind considerable damages of the financial tsunami. The current financial crisis, coupled with high inflation, would lead to lower economic growth for ASEAN countries. Cambodia will fare much better than other countries in the region of the world, due to the lack of direct exposure of Cambodian banks to the US subprime. Nevertheless, Cambodia is currently faced with two important, albeit manageable challenges: (i) indirect impact of the global financial crisis; and (ii) high inflation. I. Macroeconomic Performance in 2008

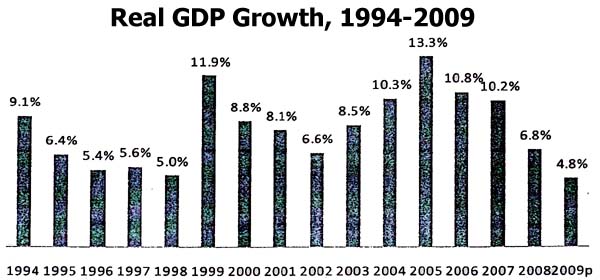

High economic growth and strong political stability that Cambodia has experienced during the last decade has been recognized by many as the “Miracles on the Mekong”. The new Royal Government of Cambodia resumes its duties in the fourth legislature with renewed dynamism and commitment to carry on its noble and historical mission with firm commitment and renewed determination to accelerate development and implementation of the comprehensive, in-depth state reform. Economic growth was robust, averaging at 9.4 percent during the last decade, 10.6% during the last five years, 2003 to 2007, with the record high of 13.3 percent in 2005, 10.8 percent in 2006 and 10.2 percent in 2007. Growth is projected to be lower at 6.8% in 2008 and 4.8% in 2009, reflecting the global economic slowdown. Inflation is expected to be 15.5% in 2008, but will be reined in to a single digit in 2009.

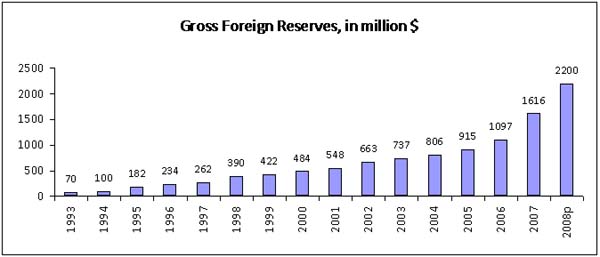

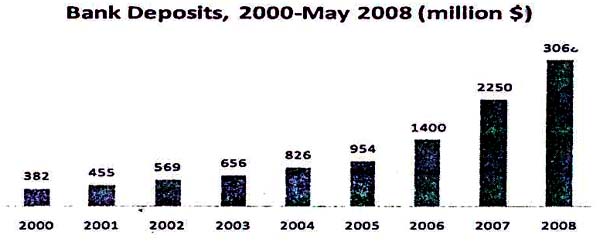

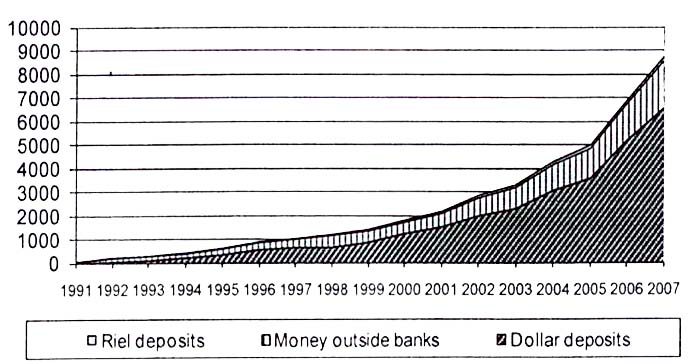

Our international resources position has been favorable and was doubled during the last two and a half years only, from $1 billion in 2006 to $2 billion in June 2008. It took 12 years for Cambodia's gross foreign reserves to increase from $100 million in 1994 to $1 billion in 2006. 1.1. The Banking Sector

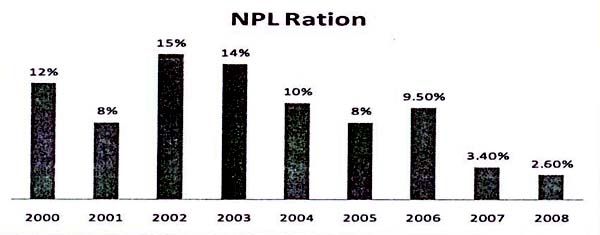

Such rapid growth poses some challenges for the banking sector: (i) the quality of loans might have degraded; (ii) the rapid expansion of the banking sector has outstretched the central bank (National Bank of Cambodia)'s capacity to supervise commercial banks; and (iii) increase exposure of banks to real estate. To sustain growth and ensure the soundness of the banking sector, the authorities have taken steps to recapitalize bank, improve prudential regulations and strengthen supervision:

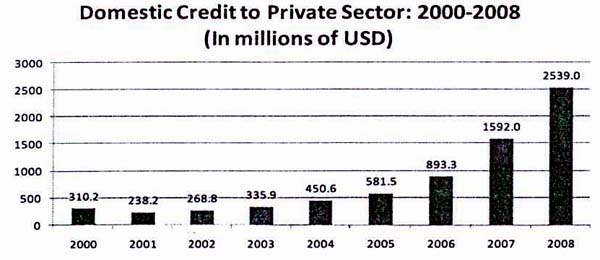

1.2. Financing Economic Growth Cambodia has witnessed increase in both foreign direct and portfolio investments during the last five years, reflecting steady improvement in investment climate and the dominant role played by the private sector in promoting social and economic development. Foreign investment funds have become more and more popular and contributed to high economic growth.

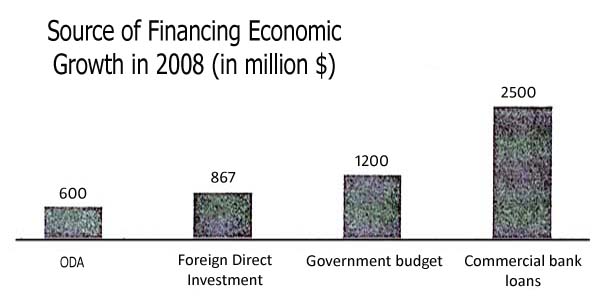

Cambodia's economic growth relies on the following for pillars:

Cambodia has set clear objectives of establishing stock and bond markets in late 2009 as stipulated in our Financial Sector Development Strategy 2006-2015. Progress has been made to improve accounting standards, ensure good corporate governance and prepare the corporate sector to be listed on the stock markets. The Royal Government of Cambodia invited Korean Exchange and foreign securities companies to come and joint it in this important endeavor. The stock market will become the fifth pillar of financing for Cambodia. II. Inflation This section is focused on:

Following are factors behind recent rise of inflation. Identifying the causes of inflation is critical for applying medicine to cure inflation. There are three major types of inflation. 2.1. Increased Capital Flows and Inflation In recent years, capital flows have played an increasingly important role in the balance of payments. Since 2005 the capital and financial account of the balance of payments rose sharply. The financial account increased by 39 percent from US$324 million in 2006 to US$451 million in 2007. The capital transfers in the form of medium and long term loans increased by 41 percent from US$123 million in 2006 to US$173 million in 2007. The influx of private capital in the form of FDI increased by 50 percent, from US$475 million in 2006 to US$711 million in 2007. The increase in investments reflects the confidence of investors in the political and macroeconomic stability of the country. FDI is considered as “non-debt creating”, because FDI does not add to external debt. Investors acquire equity in a domestic enterprise, create or expand subsidiary and there are no contractual obligations. The distinctive feature of this type of capital inflow is that it involves not only a transfer of resources, but also the acquisition of partial or full control. FDI does not create a debt obligation, and it is an important vehicle for the transfer of technical and managerial skills from abroad. The benefits of such technological transfers are often seen as outweighing the capital flow itself. In 2007 the overall the balance of payments was in surplus by US$290 million (3.4 per cent of GDP in 2007 compared with 2.8 per cent in 2006). This outcome was underpinned by the increase in tourism receipts (US$1.1 billion), the surplus of both private and official transfers (US$748 million), the increase in concessional loans, and the increase in foreign direct investment (US$711 million). The above capital flows have helped to finance large current account deficits associated with higher imports and higher economic growth. It also permitted build up of reserves. At the same time, sudden surges of these sizable inflows have caused some problems of macroeconomic management. There are the following concerns:

2.2. Demand-pull inflation Demand-pull inflation is inflation caused by increases in aggregate demand due to increased private and government spending. A surge in the demand for goods and services in general (aggregate demand) is thought to "pull" prices up across the board, especially when aggregate supply is held back by capacity limitations. A major part of demand-pull theory centers on the supply of money: inflation may be caused by an increase in the quantity of money in circulation relative to the ability of the economy to supply (its potential output);

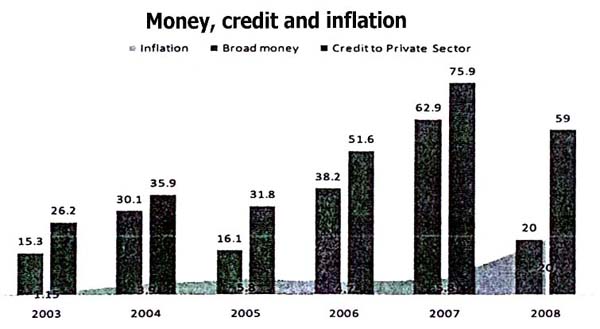

The above graph shows that there is correlation between the growth in money supply and inflation. To emphasize this thesis, Milton Friedman states that “Inflation is always and everywhere a monetary phenomenon”. This is called demand-pulled inflation.

The critical issue, however, is to determine how much inflation is caused by the increase in money supply and how much is driven by the costs, i.e. increase in energy and food prices. The above graph shows steep rise in liquidity or M2 money supply during the last five years. In response to demand-pulled inflation, the National Bank of Cambodia has taken the following monetary measures:

23. Cost-push inflation or “supply shock inflation”

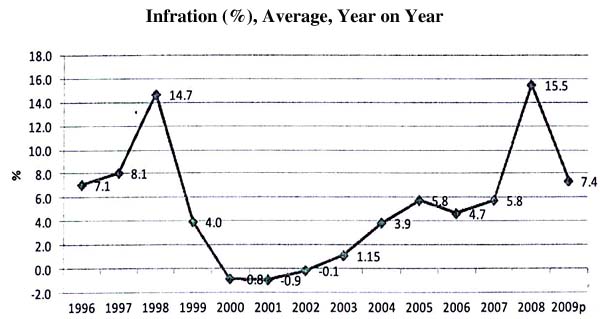

Cost-push inflation is caused by drops in aggregate supply due to increased prices of inputs. The “cost-push” factors like oil, food, monopoly profit-taking, or wages would increase the general level of prices. Producers who incur higher input costs could then pass this on to consumers in the form of increased output prices. Inflation in Cambodia starts to rise commensurately with the increase in oil prices. Inflation was zero in 2002, rising to 1.15% in 2003 and 3.9% in 2004. Oil prices on the international market started to increase in 2003. Thus, one can reasonably say that inflation in Cambodia followed the oil price.

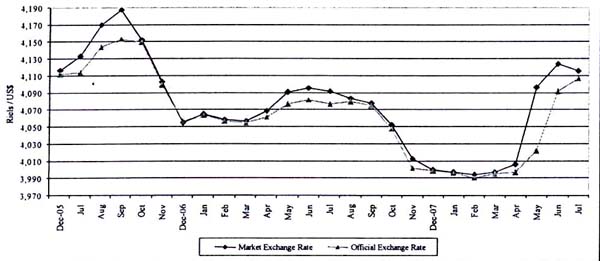

As oil prices accelerate in the second half of 2007, inflation reached 10.8% in December 2007. Higher food prices, which also accelerated in early 2008, pushed inflation further upward. Trends in Monthly Exchange Rate

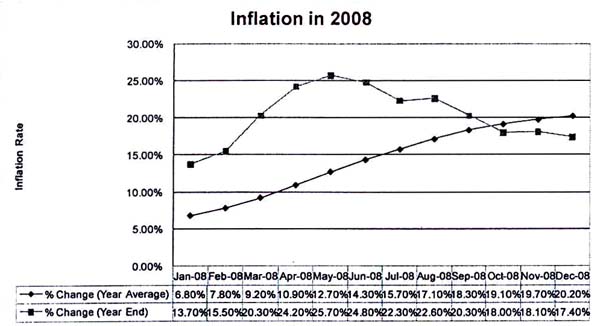

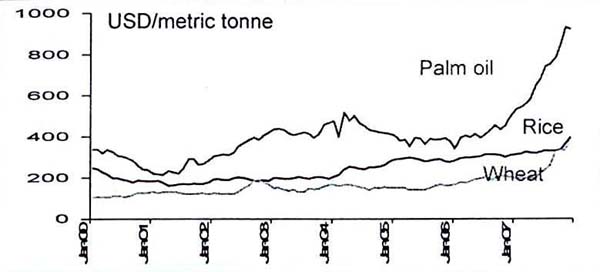

The acceleration in inflation in large part reflects the impact of higher energy and commodity prices. High inflation and in particular an increase in food prices must be taken seriously, as it creates potentially significant challenges to socio-economic stability that could undermine prospects for restoring the combination of solid growth and low inflation that Cambodia has enjoyed in the past years. World Price for Selected Food Commodities

Fiscal Policy Responses to cost-pushed inflation: Implemented Fiscal Policy Measures:

Although the above measures are mostly expansionary, the government has also taken contractionary measures to curb inflation:

2.4. Built-in Inflation Built-in inflation is induced by adaptive expectations, often linked to the "price/wage spiral" because it involves workers trying to raise their wages to keep up with higher prices (gross wages have to increase above the CPI rate to net to CPI after-tax) and employers passing higher costs on to consumers as higher prices as part of a vicious circle. Built-in inflation reflects events in the past, and so might be seen as hangover inflation. The objectives of the Government's introduced policy measures is to return the Cambodia economy to a path of strong and stable growth, accompanied by low and stable inflation. To achieve this objective in the current circumstances will require a coherent set of policy responses across a broad front. These will include structural measures designed to improve market efficiency, as well as possible monetary and fiscal policy adjustments. The challenges are great and the responsibilities in this effort inevitably will have to be shared among all concerned stakeholders. Government policies will need to be adjusted to the situation of constant price increase. Broader measures as a basis to sustaining Cambodia economic growth and prosperity will include the followings:

2.5. Additional Measures It is important to keep in mind that rising prices and inflation are challenges to economic prosperity and progress, which are potentially serious, and the Government policy responses need to be appropriate, structurally coherent and consistent in order to mitigate the impact of fuel and food prices on overall inflation and on the Cambodia macroeconomic outlook in general. Therefore additional measures have been considered as follows:

Possible measures are as follows:

2.6. Opportunities for Agricultural Development Higher food prices present also opportunities for ASEAN economies to increase investment in agriculture in order to boost productivity and exports. The economic strategy of the Royal Government of Cambodia for the fourth legislature gives priorities to the following sectors:

Cambodia will further pursue our vision of building a society which enjoys peace, political stability, security and social order, and sustainable and equitable development, with strict adherence to the principles of liberal multi-party democracy, respect for human rights and dignity, and a society in which social fabric will be strengthened to ensure that the Cambodian people are well-educated, culturally advanced, and that can enable the Cambodian people to reclaim its glory in the international arena. III. Indirect Impact of the Global Financial Crisis 3.1. The Causes of the Crisis The financial crisis started in August 2007 as a subprime crisis, which took place against the backdrop of global financial imbalances and in the context of liberalization of world financial markets. The subprime market, which experienced rapid growth during the last few years in the United States, accounted for no more than US$1,000 billion, compared with stock market capitalization of US$20,000 billion or the wealth of the American family of US$60,000 billion. The following are the factors leading to the subprime crisis:

3.2. The Developments of the Crisis Mortgage lenders distributed subprime loans to low income households, who were not eligible for prime rate loans and were known for defaulting previously contracted credits. The households were not informed that the interest rates were variable or would increase after one or two years. The mortgage lenders then resold the subprime loans to investment banks (in some cases the mortgage lenders and the investment banks are from the same group). With financial innovation, financial engineers transformed the subprime loans, via securitization, into securities, such as Mortgage-Backed Securities (MBS) or (for non-mortgage loans) into Asset-Backed Securities (ABS), then into Collateralized Debt Obligations (CDOs). The CDO made from ABS or MBS were rated by the rating agencies (Moody or S&P) by differentiating their risk profiles. Investment banks buy, for their own account or for the account of their clients, billions of CDOs from ABS, which yielded higher returns than the US Treasury Bills. To hedge against the risk, the investment banks bought insurance from specialized insurance companies (credit enhancers) or bought special securities called Credit Default Swap (CDS), issued by other investment banks. CDS have become a market on its own right. However, here this kind of risks might be uninsurable. The risk can be insurable, when insurance companies collect small premium from a large pool of policyholders to meet future liabilities, when only a few claims will occur. When interest rates started to increase from late 2006, more and more American households found out that their monthly payment were exploding. Unable to pay back the mortgage loans, they were evicted from their homes, which were then seized by banks that have sought to resell them later on. But when the number of foreclosures exploded, the real estate market collapsed. Investors who bought CDO via Mutual Funds realized that parts of the mortgages based on which the securities were made would not be redeemed. Holders of CDO attempted to get rid of them and the CDO market also collapsed. The credit enhancers who supposed to guarantee the value of the securities are unable to meet the claims and went bankrupt. The investment banks had to depreciate the value of CDOs that they hold on their books. Each bank knows the value of "toxic" CDOs they hold on their books, but ignore how much their neighbors have. By precaution, they refuse to lend money to other banks, except in case of high interest rate. Banks that rely on the inter-bank market for refinancing have become fragile. The market has become such very complex and opaque that bankruptcy of a financial institution will impact another bank through the domino effect. The banks need some time to understand and evaluate their exact exposure to these "toxic securities". Therefore, the bankruptcy of a bank sent a ripple effect to other banks that were involved with the troubled banks. 3.2. Impact of the Global Financial Crisis on the Cambodian Economy The current global financial crisis has had only indirect impact on the Cambodian economy. Cambodia's commercial banks do not have direct exposure to the subprimes. The indirect impact will be at the following levels: 3.2.1. Indirect Impact on Banks The current global financial crisis will have only limited indirect impact, if any, on Cambodian banks. The National Bank of Cambodia only recently authorized financially sound commercial banks with excess of liquidity to invest some of their assets abroad. The foreign assets of the banking system are invested abroad by the NBC in very secured financial instruments. Therefore, the exposure to the crisis only via the parent companies of some commercial banks based in Cambodia. So far there is no information that any of them have been affected by the subprime crisis. Lending is based on collateral linked to real estate. Cambodia is still a cash-based economy. The real estate market has slow downed, but there is no sign of hard landing. The measures to improve the banking system include:

Future Monetary Measures include:

The above measures that have been taken or future measures to be taken by the NBC will further strengthen the soundness of Cambodia's banking system. 3.2.2. Indirect Impact on Garment Exports Financial crisis would lead to lower consumption. The impact depends on to what extent the financial crisis will affect the real economy and how long will recession last. People therefore prefer to save money to meet difficult time ahead. The drop in consumption would further lead the economy into an economic crisis. Cambodia exports around 70% of garment products to the US. During the crisis there will be a substitution effect, shifting from the purchase of luxury goods to the mass consumption goods like Cambodian garments. As both the US and Europe are in recession, the chance is that the level of garment exports will be leveled off in 2008, compared to last year. 3.2.3. Indirect Impact on Tourism People would prefer to put off their holidays during hard times. Job losses and morose environment would be less favorable for vacations. Tourist arrivals in 2008 would grow, albeit at a slower pace compared to last year. 3.2.1. Indirect Impact on Construction The real estate market in Cambodia is stagnant since June 2008. The central bank policy to limit exposure to the real estate market managed to cool down the market and prevent the bubbles from bursting. Moreover, investors are cautious, as real estate crisis is in full swing in the US and in Vietnam. There is no sign of commercial banks exposure to the real estate problems. Garment, tourism and construction constitute 3 of the four pillars of Cambodia economic growth. Sluggish growth of the three subsectors would result in lower economic growth, estimated at 7% in 2008 and 6.5% in 2009.

|

|

Home| 2nd CDCF Meeting| 1st CDCF Meeting | Partnership and Harmonization TWG | GDCC | Policy Documents Guidelines | Aid Management Documents |