|

|

|

|

|

||

|

|

|

|

|

|

|

||

|

|

|

1. Historical background and recent trends in donor assistance Public Finance Reform before TCAP The Royal Government of Cambodia faced a sudden drop in foreign assistance from the former Eastern Bloc, mainly Russia and Vietnam, in 1989-1991. This led the government to run large budget deficits, igniting inflation which persisted at levels of more than 100 percent until 1992. In 1993, the newly established government launched the first generation of public finance reform through an Organic Budget Law. The law tightened control over public revenues and expenditures by reforming institutional arrangements, and proved effective in fighting inflation. Inflation rates started declining in 1994 and were contained below 10 percent from 1994 to 1997. Although effective in maintaining fiscal discipline, the 1993 Organic Budget Law and its institutional arrangements were not sufficient to address the other major challenges facing public financial management in Cambodia. One of the fundamental problems was that the institutional arrangements for public expenditure management were not conducive to disbursing planned budgets to spending units regularly. Another challenge was on the revenue side of the public finance. Despite the efforts at reform, Cambodia’s revenue-raising capacity has remained very weak. Its revenue-GDP ratio, for example, ranked as one of the lowest in the region. Initiation of TCAP Following the general elections in July 1998, the new government launched a program of economic reform for the period 1999-2002 aimed at supporting the reconstruction of the country, accelerating economic growth, reducing poverty, improving social conditions and preserving macroeconomic stability. This program has been supported by a Poverty Reduction and Growth Facility (PRGF) loan from the IMF totaling US$82 million, and a Structural Adjustment Credit (SAC) from the World Bank of around US$30 million. The government, however, recognized the need for substantial technical assistance to meet the reform objectives set out in the PRGF and SAC. It requested the IMF’s assistance in designing a comprehensive program of technical assistance (TA) covering key areas including macroeconomic policy, fiscal reform (tax administration and policy, customs administration, and budget management), banking reform, statistics, and legal frameworks. Following the IMF’s decision in 1999 to adopt a more programmatic approach to the planning and delivery of technical assistance to its recipient member countries, the IMF TCAP exercise (see Box 9-1) was initiated with the government in early 2000. The timing of TCAP coincided with the government’s presentation of a new development cooperation partnership paradigm to the donor community at the Consultative Group (CG) meeting (May, 2000). As described in Chapter 1, the government declared its commitment to enhancing partnerships to improve the effectiveness of development cooperation programs. The TCAP exercise was a response to the articulation of the government’s partnership paradigm.

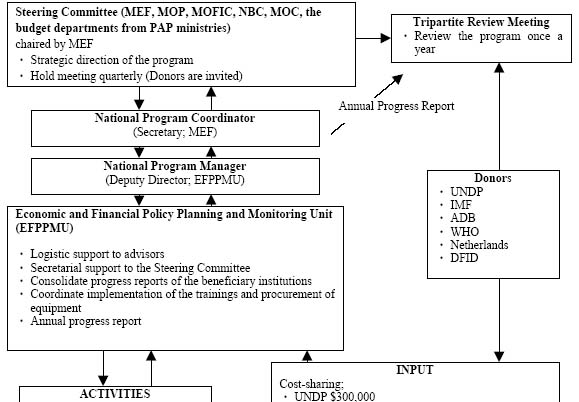

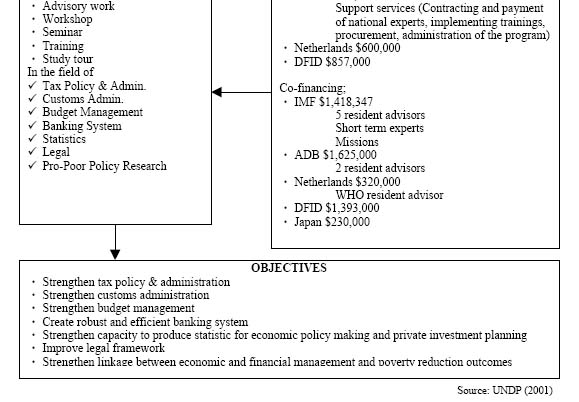

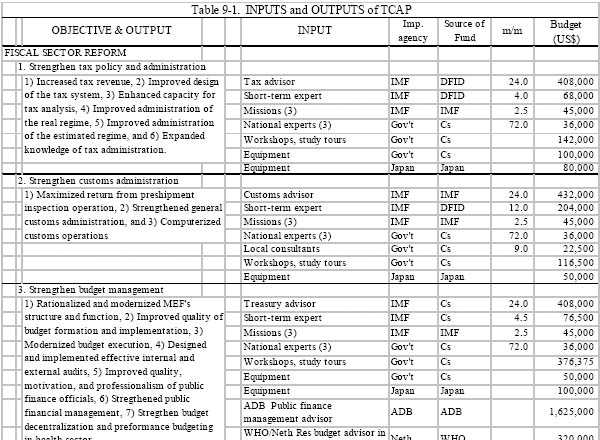

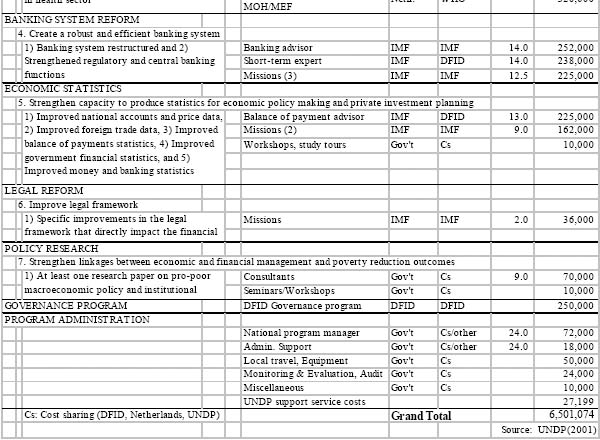

Overall program activities The TCAP program is divided into four major sub-programs and two research programs. The major sub-programs include fiscal reform, banking system reform, economic statistics, and legal reform. The two research programs are a governance program study and pro-poor policy research. Chart 9-1 presents the institutional arrangements and objectives of TCAP, and Table 9-1 summarizes the inputs and outputs of TCAP. The objectives of each sub-program are as follows:

Six key departments and agencies received assistance: Tax, Customs and Excise, and Budget Departments and Treasury at the MEF; the National Bank of Cambodia (NBC); and the National Institute of Statistics at the Ministry of Planning (MOP). Program activities include: (i) sending supervision missions; (ii) posting resident advisors; (iii) sending short-term experts; (iv) arranging seminars and training courses in Cambodia or overseas study tours; and (v) providing materials and equipment. Assistance for these activities has been provided through five IMF resident advisors in budget management, customs administration, tax administration, banking system, and economic statistics, and through visits by short-term experts and an ADB fiscal advisor. Other Externally Funded Programs Other donors also provide technical assistance in areas that have important linkages with TCAP; such as support by French Cooperation to the MEF for expanding the provincial coverage of VAT and public accounting; and support from Japan to provide technical assistance in the area of taxation and human resource development. Although not directly involved in TCAP, they have been regularly consulted by TCAP resident advisors. In particular, Japan has cooperated closely with TCAP in implementing staff training on taxation in Japan. 2. Mechanisms to manage aid coordination Institutional Arrangements Implementation of the program is guided by a Government Steering Committee chaired by the MEF (Chart 9-1). The members of this Committee consist of senior officials at MEF (from the Tax Department, the Customs and Excise Department, and the Department of Budget and Finance Affairs), NBC, Ministry of Commerce (MOC), MOP, Ministry of Foreign Affair and International Cooperation (MOFIC), and budget department officials from two Priority Action Program (PAP) ministries, i.e., Education and Health. Representatives of donor agencies are invited to Steering Committee meetings. The Steering Committee is responsible for articulating the strategic direction of the program and for ensuring that program objectives are achieved. The Committee delegates implementation responsibilities to the beneficiary institutions under TCAP. The MEF (as the executing agency) designates a National Program Coordinator who is responsible for management and administration of the program. The National Program Coordinator serves as the secretary to the Steering Committee and is responsible for coordinating assistance internally among the participating government departments and agencies, and externally with participating donors. The Steering Committee normally meets quarterly to review progress and update work plans. The National Program Coordinator reports progress to the Fiscal Reform Working Group, co-chaired by the Senior Minister of Economy and Finance and the IMF Resident Representative on a regular basis throughout the program period. The Fiscal Reform Working Group serves as a coordination institution among a broader group of donors than that under TCAP. Chart 9-1. Implementation arrangements of

The Economic and Finance Policy Planning and Monitoring Unit (EFPPMU) at the MEF is responsible for: (i) providing logistical support to resident advisors and short-term experts, and secretarial support to the Steering Committee; (ii) consolidating progress reports of various beneficiary institutions; (iii) coordinating implementation of training programs and procurement of equipment; and (iv) assisting in preparing for and reporting to annual tripartite review meetings. A National Program Manager is appointed to TCAP from the EFPPMU. In addition, the EFPPMU provides national experts82 to the Tax Department and the Custom Department for TCAP activities. The National Program Manager reports to the National Program Coordinator and external partners. The National Program Manager calls monthly meetings with TCAP resident advisors, department heads, and national experts in order to discuss the progress made, issues to be addressed, and future plans. Also the National Program Manager is responsible for compiling quarterly and annual reports. Funding and fund management The program budget over a period of three years is US$ 6.5 million. The budget includes two types of contributions, cost-sharing (using a trust fund) and co-financing. The trust fund contributions are pooled and used for the funding of short-term experts and resident advisors (e.g. Treasury advisor), salary supplements, trainings, seminars and workshops, study tours and administration costs. Co-financing contributions are arranged by each donor agency for resident advisors, short-term experts and missions. In addition, Japan provided US$230,000 for procurement of equipment. Inputs for each sub-program are summarized in Table 9-1. UNDP manages the trust fund contributed by UNDP, DFID and Netherlands. The management of the trust fund follows standard funding procedures under the UNDP national execution modality (NEX). Quarterly advance of funds to the executing agent by the UNDP country office is the standard means of funding under the NEX. Advances are made based on a forecast of quarterly expenditures, in accordance with the project work plan. Under this procedure, the government opened a special account for the program. The account is managed by the National Program Manager and receives the necessary budget quarterly from the trust fund on a request basis. The special account is subject to annual audit by independent auditors. National experts are chosen from among government officials, and are paid salary supplements from the trust fund.83 The National Program Manager is responsible for submitting reports on the work performance of the national experts, in collaboration with TCAP resident advisors.

Process of aid coordination (i) Planning TCAP was formulated according to standard IMF TCAP procedures, consisting of the three steps: (1) the sending of diagnostic and technical assistance missions; (2) presentation of a draft plan at CG meetings or special donor meetings; and (3) negotiation with donor agencies and formulation of the program. In February to April 2000, the IMF fielded a number of diagnostic and technical assistance missions to Cambodia. These mission identified technical assistance requirements as summarized in the document, Cambodia – Summary of Technical Assistance Needs in Economic and Financial Management (May 2000), and distributed at the Partnerships for Development Working Group on May 24 in Paris, prior to the Cambodia CG Meeting held on May 25-26, 2000. IMF sent two missions to Cambodia after the diagnostic and technical assistance missions to coordinate technical assistance with other bilateral and multilateral development partners. The first mission, in early June 2000, briefed local representatives of major donors on the TCAP exercise and TA needs, and explored their interest in participating in TCAP. The second mission, in July 2000, worked with the authorities and UNDP to formulate the program and draft a program document. The mission informed the Donor Working Group on Fiscal Reform, and invited interested donors to provide input to the formulation of the program. (ii) Implementation The TCAP framework consists of two components: (i) training, seminars, workshops, and study tours carried out using the trust fund; and (ii) technical assistance provided by participating donors. DFID, Netherlands and UNDP have contributed to the trust fund. IMF, ADB and WHO have provided technical assistance. The IMF is responsible for providing resident advisors and short-term experts, and carrying out technical and supervisory missions under the program’s four main components: (i) fiscal sector reform; (ii) banking system reform; (iii) economic statistics; and (iv) legal reform. ADB and WHO are responsible for providing resident advisors for public financial management and public expenditure management in the health sector, respectively. DFID, in collaboration with the National Program Coordinator and the IMF resident advisors, is responsible for the implementation of the governance program component. UNDP is responsible for implementing the pro-poor policy research component and providing support services to the government for contracting and payment of national experts, implementation of training programs, procurement of computer equipment, and local administration of the program. (iii) Monitoring, Evaluation and Review An IMF staff person monitors the work of each IMF advisor on a regular basis. TCAP IMF resident advisors submit monthly reports to the IMF staff in charge. The IMF staff replies to monthly reports and makes adjustments to the work plan whenever necessary. He also undertakes periodic inspection visits to hold discussions with advisors and with country authorities. Program evaluation is carried out through joint reviews by representatives of the government and participating donors. The UNDP resident representative, together with the Steering Committee, convenes Tripartite Review Meetings to review the program once a year. Representatives of participating donors participate in the Tripartite Review Meetings. The National Program Coordinator (with the assistance of the National Program Manager and the EFPPMU) prepares annual progress reports for the Steering Committee and other concerned parties, in consultation with inputs from UNDP and IMF. Those reports are circulated at least two weeks before Tripartite Review Meetings. The ADB advisor submits an annual progress report to the National Program Manager and ADB resident director in Cambodia. A final program evaluation is expected to be held jointly to look at outcomes and impact of the program, and to draw conclusions about future assistance. 3. Achievements of aid coordination The formal evaluation of TCAP program is expected to be conducted by independent evaluators in the near future. The current study, therefore, should not be interpreted as the formal program evaluation. It aims to provide an interim assessment of what has been achieved in some key aspects of aid coordination; namely, local ownership, local capacity, overlap of assistance, transaction costs to the government, and sustainability. Local ownership Under the supervision of the National Program Coordinator, the National Program Manager and national experts team have played a critical role in managing the program, taking the initiative to implement the program and coordinate various departments and donor agencies involved. Many interviewees reported that the presence of local ownership was manifested in active attitudes of the Manager and the national expert team. However, ownership within the departments that have received training appears to have been weak. It was reported that TCAP resident advisors had prepared most of reform documents and these activities have been donor-driven. The participation of department managers in the training program was not as active as desired, and they tended to rely on advisors for implementing reform initiatives. An annual progress report of TCAP highlighted this point, noting that "…while the recent management workshops exposed managerial staff to the reform program, to date only a relatively small number of senior officials actively participate in it. While the provision of a resident advisor has been helpful to date, there is a tendency for managers to rely on him to take more leading role in implementing the reform initiatives than is desired."89 This point was also confirmed by three TCAP resident advisors who were interviewed for this study. Capacity enhancement It was reported that the National Program Manager and national expert team have gained good experience from managing the TCAP program. They felt that they could use their new skills if any similar opportunities arise in the future. However, this experience largely belongs to the individuals and it is not immediately clear whether institutional capacity has been enhanced. At present, it appears that the experience and capacity gained through the program is unlikely to be used once the National Program Manager and national expert staff team are returned to their regular assignments. Overlap of donor assistance The TCAP has enhanced information sharing and coordination among donors, has helped eliminate overlap of assistance in the broad area of public financial reform, and maintained consistency and synergy among the activities conducted in different departments. Before TCAP, IMF and ADB provided technical assistance to various fields of fiscal reform independently without much coordination. With the introduction of TCAP, however, the opportunity to exchange information among TCAP resident advisors and among departments which are physically dispersed has been expanded considerably. In addition, technical meetings under TCAP have been held monthly, involving advisors and representatives of each department. Through the various meetings, TCAP resident advisors could confirm their activities and the overall objectives, and maintain consistency among the activities. In addition, TCAP resident advisors have been voluntarily holding weekly meetings to exchange information and views on program activities. This kind of opportunity would not have been possible without TCAP. Transaction costs to the government The transaction costs to the government to coordinate donors could have been much higher if each component under TCAP had been planned and managed separately with different donor agencies. In this sense, the transaction costs to the government, especially at the planning stage, were reduced through TCAP. It was reported that TCAP has placed heavy transaction costs on participating donors, in terms of substantial staff resources used to coordinate donors in planning, implementation, monitoring and evaluation. However, considering the benefits brought by TCAP, participating donors seem to have been willing to pay this extra cost. Sustainability The sustainability of achievements under TCAP will depend on government ownership and perseverance in implementing actions started under TCAP. The implementation of some actions would take time and require enduring commitment by the authorities. Sustainability will also depend on further technical assistance. Although the TCAP, which was undertaken on a pilot basis, is coming to an end during the first quarter of 2004, technical assistance will be provided by the IMF (and other donors) in the key areas of public finance targeted under TCAP. The TCAP has produced a number of substantial outputs, including, among others: (i) a draft customs law for customs administration and the statistics law and sub-decrees for economic statistics; (ii) the creation of a Large Tax Unit and a Medium Tax Unit for tax administration; (iii) the establishment of a Cash Management Committee; (iv) Manuals for Tax Collection; and (v) Standardized Accounting Procedures for Treasury Management. However, these achievements are only the first step in the long reform process. For instance, the Manuals for Tax Collection and the Standard Accounting Procedures for Treasury Management would apparently need to be tested and used for capacity building activities in the years to come. If there is no follow up activities, those achievements might have only a limited impact. The MEF’s experience to manage aid coordination through TCAP should not be under-utilized. 4. Lessons from aid coordination Contributing factors to achievements The broad, comprehensive framework of the program helps enhance coherence and complementarity among donor assistance. TCAP has been one of the main instruments for the implementation of public finance reform in the last few years. With the government-donor partnerships, TCAP has been able to cover a broad area of reforms and restructured the administration of related government units. Therefore, TCAP has had a significant influence on financial management on the whole. Before TCAP, donor assistance was given in the form of individual projects by different donors and the impact was scattered and less coherent. Now, a large part of capacity building activities are carried out under the TCAP framework. As a result, the overlap of assistance has been largely eliminated in this area. Institutional arrangements should be flexible to accommodate local needs. Procedures or management systems should be modified if they turn out to be non-functional. For example, TCAP experienced a delay in the disbursement of the trust fund at the beginning. This was mainly because the Program Manager was not a full time position, and therefore was not able to allocate sufficient time to swiftly fulfill the conditions required for the disbursement of the trust fund. The delay in disbursement affected procurement of goods and services required for program activities and caused frustration to all involved. To address the problem, the government and its partners agreed to make the Program Manager position into full-time to work for day-to-day management of the program. The newly appointed Manager fulfilled the required conditions successfully and, as a result the program implementation has become much smoother. In short, the government and its partners modified the initial institutional arrangements to accommodate local needs, which helped improve management of the program. This may also be seen as an example of learning-by-doing. Informal networks can supplement formal mechanisms of coordination among donors. Under TCAP framework, the formal institutional arrangement of coordination among donors has been supplemented by informal networks created by TCAP resident advisors. As mentioned in section 3, TCAP resident advisors held own meetings voluntarily to exchange information and views on the program activities. This helped improve coordination of activities and management of the program. Furthermore, the TCAP resident advisors for tax administration and statistics acted as de-facto coordinators with other donors supporting fiscal reform outside of the TCAP framework.90 Their efforts helped avoid any overlap with other donors' activities and maintained good relationships, then supplemented the formal mechanisms such as the Fiscal Reform Working Group.Key issues and challenges Build on TCAP’s accomplishments TCAP has brought a new program approach to economic and public finance reform for the first time in Cambodia. Through the TCAP, the MEF has gained experience and capacity in coordinating a wide range of technical assistance activities in this area. The TCAP has produced a number of substantive outputs, which have made a critical impact on public finance reform, and laid the foundation for future activities. The challenge here is how to build on what has been accomplished under TCAP. In the preparation of a new program at the next stage, the following issues that have emerged in this study might be worth consideration: (i) expanding capacity development activities to line ministries and provinces; (ii) operationalizing the outputs produced under TCAP; and (iii) considering recipients’ views in the design of technical assistance program. (i) Expanding capacity development activities to line ministries and provinces: Training activities under TCAP have focused mainly on government officials at the national level, with the exception of some seminars on treasury management for provincial treasurers (held twice). The involvement of line ministries has been also limited, with the exception of the budget departments of PAP ministries. As our case studies in Education (Chapter 6) and Health (Chapter 7) made clear, capacity development of public financial management is needed throughout the government and especially at the sub-national level. Therefore, a new program in the next phase should consider expanding capacity development activities to other line ministries and provinces. (ii) Operationalize the outputs produced under TCAP: TCAP has produced substantial materials as listed in the previous section. These outputs, in particular the Manuals on Tax Administration and the Standard Accounting Procedures on Treasury Management, should be tested and used for capacity development activities for all government officials concerned. (iii) Consider recipients’ views in the design of technical assistance: The government officials involved in TCAP have generally appreciated the works of technical advisors, but they also suggested that recipients’ views should be considered in the design of future technical assistance. The main points which emerged from a group interview with national experts working for TCAP and other interviews are summarized in the following:

Acknowledge contribution of government officials properly: Although some advice provided by foreign advisors is based on suggestions by government officials, the contributions of the latter are often not acknowledged properly. Foreign advisors and government officials are expected to work together to achieve common program objectives. It is suggested that foreign advisors consider reporting their outputs jointly with national officers to senior management of ministries. Put capacity building first: TA programs should pay much more attention to capacity building of government officials.; Give options in the selection of advisors: It would be better if donors nominate two or more candidates for an advisor’s position and allow the government to select the most suitable person for the position. Salary supplements Salary supplements are provided for the government officials who work as national experts for TCAP, as was mentioned in Section 2. The government officials interviewed questioned whether the current level of salary supplements may undervalue the capacity of national experts. They argue that many donors assume that the capacity of all government officials is equally "poor," but this is no longer the case because a number of government officials have significantly improved their capacity through work experience and training in the last decade. According to their view, the current standard of salary supplements, which was set by the UN a long time ago, does not adequately reflect their enhanced capacity. References IMF (2002). Review of Technical Assistance Policy and Experience. Washington D.C.: Office of Technical Assistant Management, IMF. IMF (2003). Cambodia: Staff Report for the 2002 Article IV Consultation and Sixth Review under the Poverty Reduction and Growth Facility (Country Report No. 03/58). Washington, D.C.: IMF. Kato, T., Kaplan, J.A., Chan, S., and Real, S. (2000). Cambodia: Enhancing Governance for Sustainable Development. Manila: Asian Development Bank. Royal Government of Cambodia (2000). A New Development Cooperation Partnership Paradigm for Cambodia. Paper presented by H.E. Keat Chhon, Senior Minister and Minister of Economy and Finance, at the Consultative Group Meeting for Cambodia, Paris, France, 24-26 May 2000. Royal Government of Cambodia (2002). Strengthening Economic and Financial Management Project: Technical Cooperation Assistance Program (Annual Progress Report Feb.2002-Feb.2003). Phnom Penh: Economic and Financial Policy Planning and Monitoring Unit, Ministry of Economy and Finance. UNDP (2001). Strengthening Economic and Financial Management (Program Support Document CMB/00/006/B/01/99). UNDP. |

|||||||